What is the state of the feed industry in 2016?

Some 68% of respondents saw labor as an issue. “The biggest challenge for the industry is finding quality employees,” commented one participant.

Input prices topped another pollster’s list of hurdles that the feed industry must overcome, with the lack of skilled labor second in that catalogue of challenges.

Another respondent questioned how tuned in the academic sector was to the current needs of the feed manufacturing industry: “Those with degrees obtained in the last 10 to 15 years appear to be less knowledgeable than previous generations of graduates,” he wrote.

But knowledge gaps are one thing, quite another is the limited take-up of graduates joining the field:

FEFAC general secretary, Alexander Döring, speaking to this publication recently, decried the lack of new entrants into the industry, despite, he continued, it being a sector that provides “a challenging working environment” and one that offers real “prospects” for ambitious graduates.

“As is the case with agriculture in general, the feed industry is seeing a decreasing level of interest from young people to [come and] work in our sector,” said Döring.

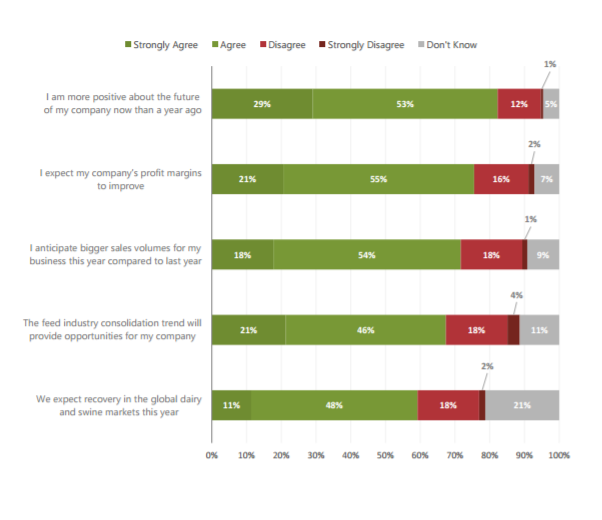

Optimism is the dominant mood though….

A clear majority of this year’s survey respondents (82%), however, are positive about the future of their companies when compared to 2015, while 67% of those polled strongly agreed that a higher degree of market concentration will provide opportunities for their firms.

“Fewer and bigger customers are both opportunities and risks. The larger the customer, the more they want a unique solution,” cautioned one reader however.

Meanwhile, 74% of our survey respondents agreed retailers and processors are increasingly dictating the agenda in the value chain.

These sentiments were echoed, back in June, by Richard Maatman, global marketing director at Trouw Nutrition, Nutreco's animal nutrition business. He told us then how the amalgamation trend was shaping the EU agribusiness landscape.

“The number of players has been declining over the past few years as a consequence of consolidation. Nevertheless, the EU feed sector remains rather fragmented. When you consider that ForFarmers, for example, is one of the largest EU compound feed companies, producing somewhere in the region of 8 to 10 million tons of feed annually, it only enjoys a 4.3% share of the European feed market,” said Maatman.

He foresaw a model developing over the next five years whereby, in each European country, there would be around three feed producers that dominate the landscape, and co-existing alongside those big players would be small scale feed mills that would serve a niche demand or would remain very specialized, producing feed for a certain (sub)species, or for organic production.

And processors will likely hold sway: “The way I see trends playing out, the long term consequences of consolidation in the EU agribusiness sector will be that the processors like Friesland Campina, who are driving sectoral change, will become the orchestrators of the value chain from feed to shelf.

“They will set the requirements, the conditions for other parties in that chain to meet, such as sustainable soy sourcing, and the feed sector will have to adapt to that. So a more concentrated feed sector would be a stronger one in terms of negotiating position, and would be more appealing, in terms of collaboration, for the large processors,” said Maatman.

Price volatility, weather

Ninety-three percent of those polled unanimously agreed there is a need for greater traceability in the global feed sector, while controlling pricing volatility and ensuring security of raw material supplies is higher up on companies’ agendas than sustainable sourcing.

“Fluctuations in prices” of raw feed materials threaten profitability, wrote one respondent.

The high price of inputs can affect feed quality, commented another survey participant.

Weather patterns and how they affect production and pricing was repeatedly mentioned as a trend to keep an eye on.

“Currency instability is a major impediment, and unpredictable weather,” claimed a reader polled this year.

Consolidation on the supply side will “create an increasingly competitive landscape moving forward. Economies in developing markets and, also, changing weather patterns around the globe will have significant impact on the industry as whole,” noted another.

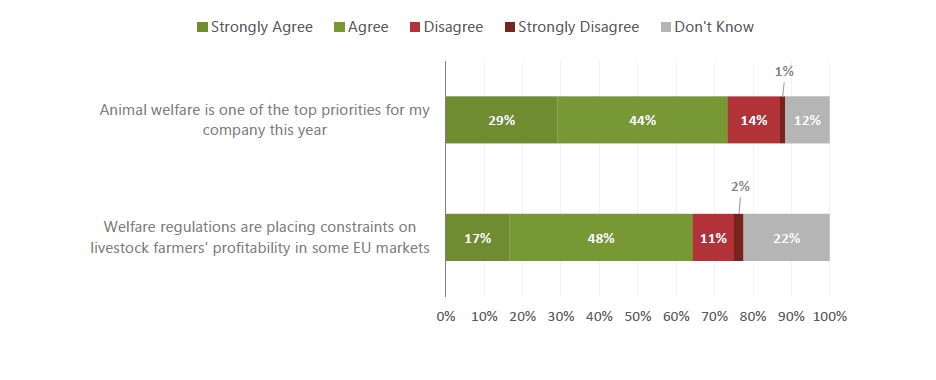

Welfare concerns

A majority of survey respondents (73%) stated that animal welfare is important but, on the contrary, 65% of participants said welfare regulations were hampering livestock sector growth in some EU countries.

“The rules of engagement and directives can change with increasing consumer and food safety groups challenging the whole animal protein production industry,” wrote one survey respondent.

Another participant said: “The influence of the ill-informed consumer is felt across the industry" but that development was only resulting in an increase in costs while bringing "no improvements in quality, food safety or sustainability.”

In May this year, Henk Flipsen, director of the Dutch feed trade group, Nevedi, told us there was, undoubtedly, a serious economic crisis in the Dutch pig sector, exacerbated by the Russian boycott and low international pork prices.

But he stressed Dutch pig producers have to pay higher costs than their EU counterparts in areas such as manure, environmental measures and animal welfare and these outlays are playing havoc with their profitability: “Some of these welfare policies are politically motivated, aiming to meet unrealistic consumer expectations, and are also based on an agenda that aims to put an end to intensive pig farming in the Netherlands.”

He said Dutch pig farmers, which used to be among the most competitive in the EU, are also confronted with intense pressure to use certified ingredients such as soy.

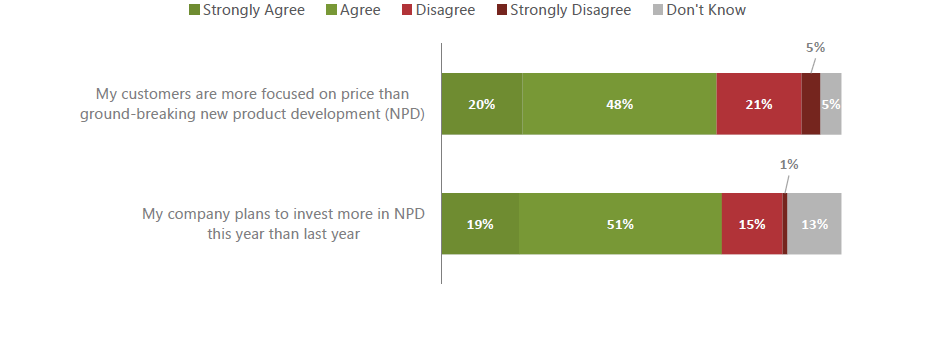

Innovation

Seventy percent of survey respondents (▲12% from last year) agreed their companies were planning to invest more in NPD this year. However, 68% of respondents also agreed their customers were focused more on price than ground-breaking product development.

“I would say that NPD is one of the major concerns of all of us and, with that being true, the need to have sufficient funds available to be successful in a NPD program is first on the list [of must haves] with having staff capable to run these development programs [coming a close second],” said one survey participant.

One participant stressed there was a need for more NPD focus on products that allow for efficient feed digestion in the rumen to enable enhanced nutrient absorption in cattle.

Someone else noted the difficulty in generating investment for new technology, while another reader said “the length of time involved to register new innovation” was hampering sector growth.

One respondent reported how low milk prices had forced their business to become more innovative.

Another participant cited as a negative trend the “crowded field in gut health, with the resulting commoditization of some products as more and more suppliers enter the arena.”

And a respondent noted that “low prices in the additive business” were proving a barrier to NPD generally.

Antibiotic reduction and the hunt for alternatives to such drugs comes across, from the comments, as a common industry NPD driver. One reader, though, complained there remains few suitable, economically viable antibiotic replacement products to choose from.

Brexit fallout

Regulatory burdens were cited as significant hindrances to growth by many respondents.

And uncertainty around Brexit was also mentioned as a concern for the feed sector and beyond:

“We are concerned about the effect of the UK planning to leave the EU on a number of issues including client and investor opportunities, willingness to invest in infrastructure in a time of uncertainty, retention of non-UK EU staff, and impact of currency fluctuations on planned equipment purchases, etc.”

The FeedNavigator State of the Industry Report 2016 can be downloaded here